amortization

Content

For example, you can enter 60 to amortize the amount over 60 periods starting from the amortization start date. You can recognize different amounts to different accounts within the same period when you set several lines to the same period offset value. Straight-line, using exact days – amortizes amounts individually for each period based on the number of days in each period. Because each day in the term recognizes an equal amount, each period may recognize a different amount. Amortization and depreciation are similar in that they both support the GAAP matching principle of recognizing expenses in the same period as the revenue they help generate.

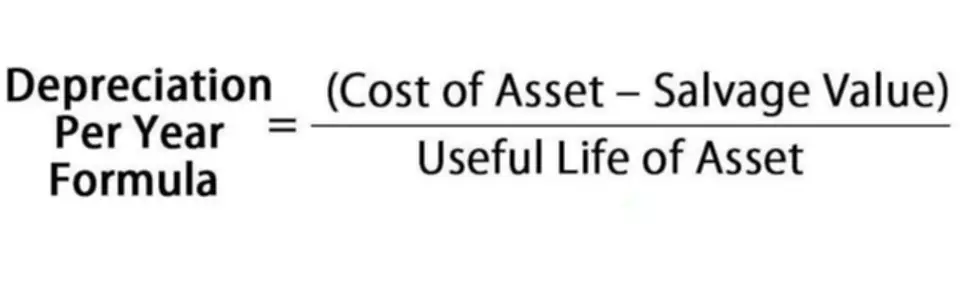

A referral to a stock or commodity is not an indication to buy or sell that stock or commodity. Ross Cameron’s experience with trading is not typical, nor is the experience of traders featured in testimonials. Becoming an experienced trader takes hard work, dedication and a significant amount of time. Get up and running with free payroll setup, and enjoy free expert support. Residual value is the amount the asset will be worth after you’re done using it. Of its debt; and by 1852 the revenue exceeded three million dollars annually.

What Is Negative Amortization?

Amortization is important because it helps businesses and investors understand and forecast their costs over time. It is also useful for future planning to understand what a company’s future debt balance will be in the future after a series of payments have already been made.

- Your scheduled payments — These are the monthly payments you are required to make.

- Retailers that own facilities generally view them as long-term investments and amortize them over thirty to fifty years.

- Were loosened in the 1990s and 2000s, the IRS often insisted that assets could only be amortized if they had a real, finite lifespan and actually lost value over time.

- By amortizing the cost of the reversal over those insertions, we see that each operation requires only 0 amortized time.

- You can also use the formulas we included to help with accurate calculations.

- Period Offset moves the entire amortization period ahead by the number of periods you specify, keeping the same number of periods.

Readers are encouraged to develop an actual amortization schedule, which will allow them to see exactly how they work. For straight amortization without extra payments, use calculator 8a.

Amortizing a loan

This ending balance will be the beginning balance of the next month. Repeat steps two through four for each month of your amortization schedule. If you’re calculating your amortization table yourself, you can check your math withan amortization schedule calculator. Again, to calculate amortization your monthly interest rate, divide your annual interest rate by 12. If you apply for any of these types of loans, don’t expect an amortization schedule. Amortization in loans and bonds is a method of establishing fixed payments for the entire duration of the loan or bond.

It also serves as an incentive for the loan recipient to get the loan paid off in full. As time progresses, more of each payment made goes toward the principal balance of the loan, meaning less and less goes toward interest. Negative amortization is when the size of a debt increases with each payment, even if you pay on time. This happens because the interest on the loan is greater than the amount of each payment. Negative amortization is particularly dangerous with credit cards, whose interest rates can be as high as 20% or even 30%. In order to avoid owing more money later, it is important to avoid over-borrowing and to pay your debts as quickly as possible. Though you usually calculate the payment amount before calculating interest and principal, payment is equal to the sum of principal and interest.

Amortization & Depreciation

These details are usually outlined as soon as you take out the principal. When this happens it can be fairly easy to calculate exactly what you need. Your scheduled payments — These are the monthly payments you are required to make. They will usually be organized by month and listed individually for the entire length of the loan. Amortization is a process to spread out certain loans into fixed payments. You pay these amounts off monthly until the end of the payment schedule. Amortization also refers to the repayment of a loan principal over the loan period.

You can also find the total of the principal payments and interest for your entire loan balance in the last line of your amortization schedule. Having longer-term amortization means you will typically have smaller monthly payments. However, you might also incur brighter total interest costs over the total lifespan of the loan. Your interest expenses — When you make a scheduled payment, a certain amount goes toward your interest month by month. This ends up getting calculated by multiplying your monthly interest rate by the remaining loan balance. Record amortization expenses on the income statement under a line item called “depreciation and amortization.” Debit the amortization expense to increase the asset account and reduce revenue.

An amortization schedule will be provided when you close on a loan. With the right information, creating one yourself in Excel or a comparable program can save you some time when you’re still deciding on https://www.bookstime.com/ a loan. To calculate this ending balance, subtract the amount of principal you paid that month from the balance of your loan. Use a spreadsheet to create an amortization table and analyze your loan.

What are two types of amortization?

- Full amortization with a fixed rate.

- Full amortization with a variable rate.

- Full amortization with deferred interest.

- Partial amortization with a balloon payment.

- Negative amortization.

Amortization simplifies the borrowing process by allowing the borrower to budget for fixed payments over the entire length of the loan or bond. The best way to understand amortization is by reviewing an amortization table. If you have a mortgage, the table was included with your loan documents. After the calculations, you would end up with a monthly payment of around $664. A portion of that monthly payment is going to go directly to interest and the remaining will go directly towards the principal. However, the amount that goes towards principal will increase as the amount of interest decreases.

Recent Comments